Navigating Change: Key Tourism Sector Strategy in 2026

Tourism remains a major economic contributor to Indonesia. In 2025, the sector accounted for approximately 4.7% of GDP, generated an estimated Rp1.2 trillion in economic value, and recorded a 56% year‑on‑year increase in investment to Rp73.55 trillion. International arrivals reached 15.39 million, surpassing the government’s target and growing 10.8% compared to 2024.

Despite this strong performance, global tourism faces ongoing structural risks from geopolitical tensions and economic uncertainty. Looking ahead to 2026, pressure on long‑haul travel—particularly from the Middle East, the Americas, and Europe—is expected to persist, echoing demand volatility experienced during the pandemic period. In response, we see the potentials of Indonesia’s national tourism strategy to emphasize on strengthening the domestic market while prioritizing international growth from Asia‑Pacific source markets, notably China, India, and Southeast Asia.

Despite this strong performance, global tourism faces ongoing structural risks from geopolitical tensions and economic uncertainty. Looking ahead to 2026, pressure on long‑haul travel—particularly from the Middle East, the Americas, and Europe—is expected to persist, echoing demand volatility experienced during the pandemic period. In response, we see the potentials of Indonesia’s national tourism strategy to emphasize on strengthening the domestic market while prioritizing international growth from Asia‑Pacific source markets, notably China, India, and Southeast Asia.

1. Tourism Destination

Bali remains Indonesia’s primary tourism destination. However, to reduce over‑dependence on Bali and support more balanced regional development, the government has launched several integrated tourism destinations across the country. These initiatives aim to diversify tourism offerings, promote higher‑quality tourism experiences, and ensure a more equitable distribution of economic benefits nationwide.

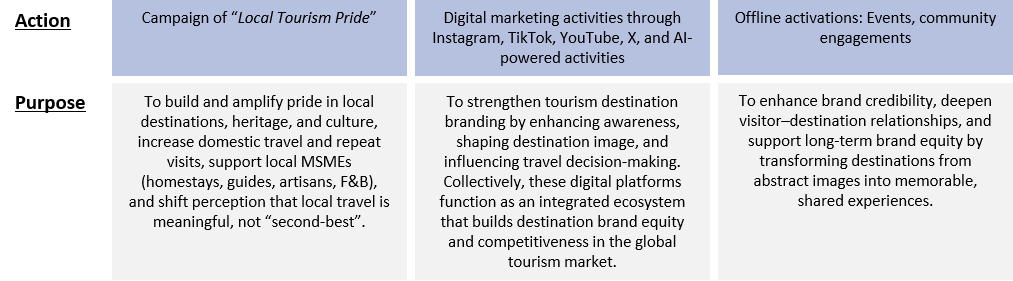

As Indonesia refocuses on domestic travelers and Asia‑Pacific visitors, tourism destinations must adopt clearer and more assertive strategies. The emphasis should shift toward actively capturing, retaining, and monetizing demand by aligning destination positioning, product development, and promotion with the preferences of these core markets.

Bali remains Indonesia’s primary tourism destination. However, to reduce over‑dependence on Bali and support more balanced regional development, the government has launched several integrated tourism destinations across the country. These initiatives aim to diversify tourism offerings, promote higher‑quality tourism experiences, and ensure a more equitable distribution of economic benefits nationwide.

As Indonesia refocuses on domestic travelers and Asia‑Pacific visitors, tourism destinations must adopt clearer and more assertive strategies. The emphasis should shift toward actively capturing, retaining, and monetizing demand by aligning destination positioning, product development, and promotion with the preferences of these core markets.

2. Hospitality (Hotels & Accommodations)

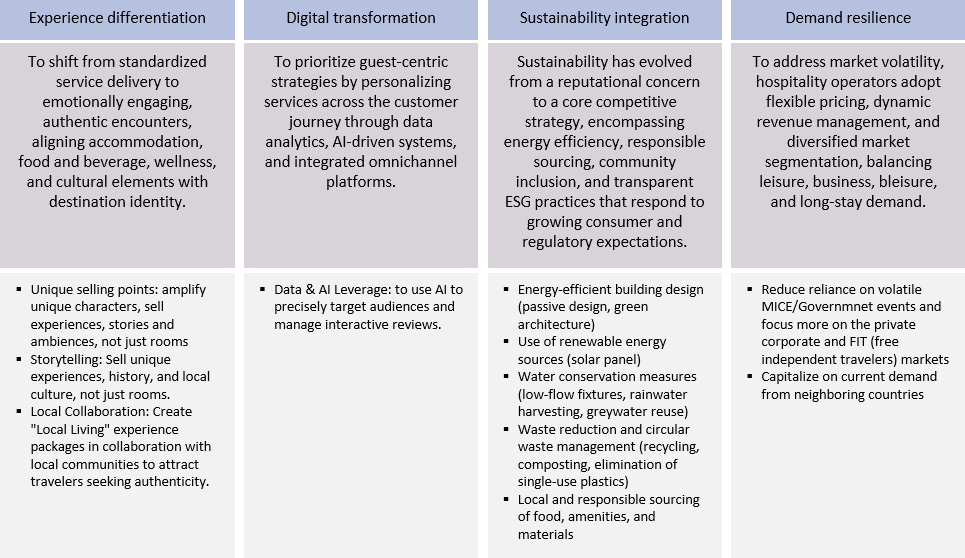

Experience‑led branding has emerged as a central strategic imperative in Indonesia’s increasingly competitive hospitality market. While overall sector expansion remains robust, supply growth in key destinations—particularly Bali and Jakarta—is now outpacing demand, accelerating risks of price compression and asset commoditization, especially among undifferentiated properties.

As competition shifts from capacity addition to brand and product differentiation, experience‑driven hotels are better positioned to preserve pricing power, guest loyalty, and revenue stability. Assets competing primarily on price face heightened exposure to OTA‑led discounting and declining RevPAR as market saturation intensifies.

Recent market dynamics reinforce this structural shift. The Indonesian hospitality sector is projected to add approximately USD 7.78 billion between 2023 and 2028, growing at a 6.2% CAGR, with demand increasingly shaped by preferences for authentic, locally grounded experiences rather than standardized accommodation. Concurrently, post‑pandemic recovery has lifted international arrivals above 15 million in 2025, alongside government‑supported destination development beyond Bali, including Mandalika, Labuan Bajo, and Lake Toba. In these emerging destinations, experiential hotels increasingly function as destination anchors, capturing both visitor and local spend while mitigating seasonality and competitive price pressures.

From an investment perspective, commoditization remains the principal downside risk in supply‑expanding markets. Experience‑differentiated assets typically demonstrate stronger ADR resilience, higher repeat visitation, and greater ancillary revenue contribution, supporting more stable cash flows and more compelling exit narratives than price‑led hotel formats.

Overall, hospitality strategies entering 2026 reflect a shift toward value‑driven, technology‑enabled, and purpose‑oriented models, emphasizing brand equity and long‑term resilience over short‑term operational efficiency.

Experience‑led branding has emerged as a central strategic imperative in Indonesia’s increasingly competitive hospitality market. While overall sector expansion remains robust, supply growth in key destinations—particularly Bali and Jakarta—is now outpacing demand, accelerating risks of price compression and asset commoditization, especially among undifferentiated properties.

As competition shifts from capacity addition to brand and product differentiation, experience‑driven hotels are better positioned to preserve pricing power, guest loyalty, and revenue stability. Assets competing primarily on price face heightened exposure to OTA‑led discounting and declining RevPAR as market saturation intensifies.

Recent market dynamics reinforce this structural shift. The Indonesian hospitality sector is projected to add approximately USD 7.78 billion between 2023 and 2028, growing at a 6.2% CAGR, with demand increasingly shaped by preferences for authentic, locally grounded experiences rather than standardized accommodation. Concurrently, post‑pandemic recovery has lifted international arrivals above 15 million in 2025, alongside government‑supported destination development beyond Bali, including Mandalika, Labuan Bajo, and Lake Toba. In these emerging destinations, experiential hotels increasingly function as destination anchors, capturing both visitor and local spend while mitigating seasonality and competitive price pressures.

From an investment perspective, commoditization remains the principal downside risk in supply‑expanding markets. Experience‑differentiated assets typically demonstrate stronger ADR resilience, higher repeat visitation, and greater ancillary revenue contribution, supporting more stable cash flows and more compelling exit narratives than price‑led hotel formats.

Overall, hospitality strategies entering 2026 reflect a shift toward value‑driven, technology‑enabled, and purpose‑oriented models, emphasizing brand equity and long‑term resilience over short‑term operational efficiency.

Several strategy in hospitality sector in the current market:

Outlook

Despite persistent geopolitical tensions in the Middle East and the United States that continue to weigh on global tourism demand, Indonesia’s tourism and hospitality sector is well positioned to navigate these challenges. Success will depend on the implementation of clear, flexible, and market‑responsive strategies, underpinned by ongoing government support and policy continuity.

Indonesia’s favorable macroeconomic fundamentals—including stable economic growth, controlled inflation, and strong domestic consumption—provide an important buffer against external shocks. As a result, the impact of global volatility on the tourism and hospitality sector is expected to be manageable and ultimately temporary, reinforcing the sector’s medium‑ to long‑term growth outlook.

Despite persistent geopolitical tensions in the Middle East and the United States that continue to weigh on global tourism demand, Indonesia’s tourism and hospitality sector is well positioned to navigate these challenges. Success will depend on the implementation of clear, flexible, and market‑responsive strategies, underpinned by ongoing government support and policy continuity.

Indonesia’s favorable macroeconomic fundamentals—including stable economic growth, controlled inflation, and strong domestic consumption—provide an important buffer against external shocks. As a result, the impact of global volatility on the tourism and hospitality sector is expected to be manageable and ultimately temporary, reinforcing the sector’s medium‑ to long‑term growth outlook.

Author

Fitrah Avianti

Principal/Lead Consultant

Principal/Lead Consultant

* This publication is also available in pdf version. Subscribe or contact us to have the report emailed.